Traditional Financial Institutions Launch Counter-Offensive in Stablecoin Market

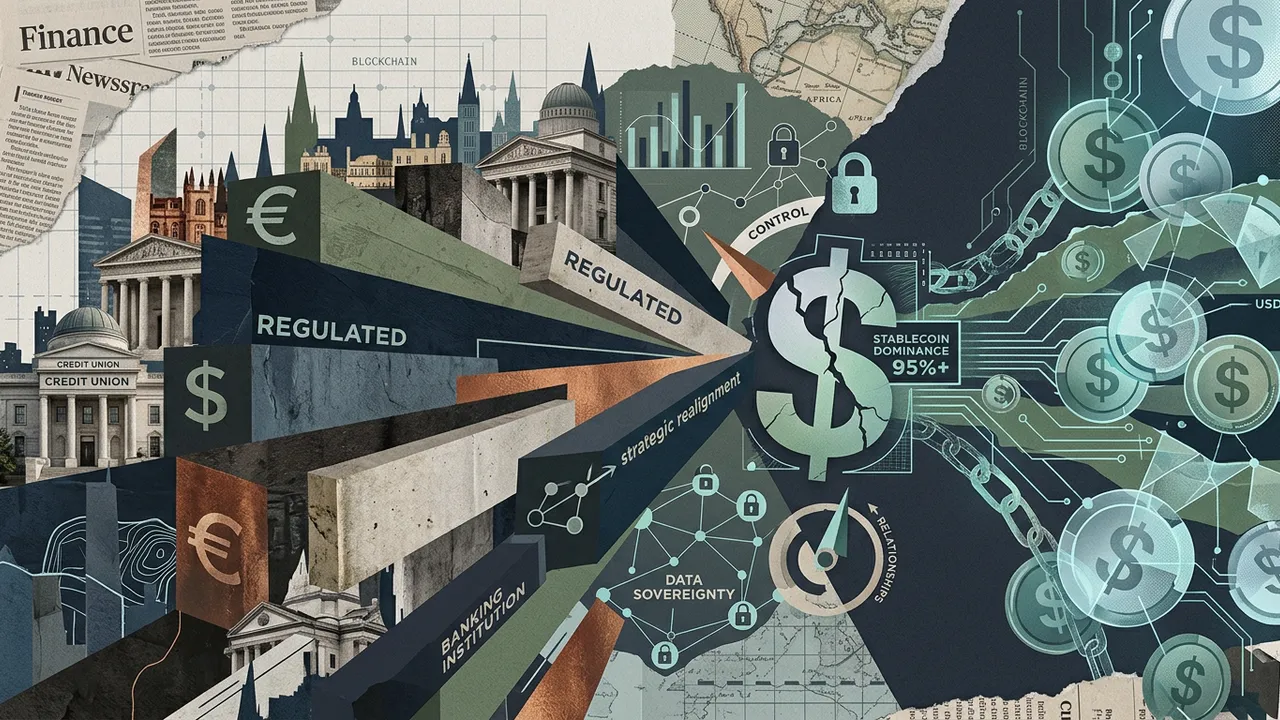

While US dollar stablecoins dominate over 95 percent of the market, European major banks and American credit unions are positioning themselves with their own digital asset solutions. Control over customer relationships and data sovereignty is at the center of this strategic realignment.

Traditional Financial Institutions Fight for Relevance in Digital Currency Market

The established financial world has recognized that digital assets are not a passing fad, but are becoming critical infrastructure. Two recent developments exemplify how differently traditional financial institutions are responding to this challenge: While twelve European major banks aim to break dollar dominance with a euro stablecoin, an American credit union is integrating Bitcoin directly into its core banking systems. Both approaches pursue the same goal—not losing control over customer relationships and digital assets to third-party providers.

The central question is no longer whether traditional financial institutions will offer digital assets, but how they will do so without endangering their strategic position. These developments mark a turning point in the integration of blockchain technology into the established financial system.

The Facts

St. Cloud Financial Credit Union (SCFCU) launched its "CU-Digital Asset Vault" for members in February 2026—a platform that integrates digital assets like Bitcoin directly into the credit union's core banking systems [1]. What makes this solution special: Unlike many existing digital asset services that outsource wallets and thus control over customer relationships, deposits, and data to external providers, the credit union retains complete control [1].

The technical foundation is provided by DaLand's CUSO's Coin2Core architecture, which connects digital asset activities with existing infrastructure. "Traditional vendor wallets pull deposits and member relationships away from the credit union. Coin2Core connects digital asset activity to the core and enables credit unions to remain trusted custodians and service providers while simultaneously supporting digital asset ownership," explained Jon Ungerland, CIO of DaLand CUSO [1]. Members retain control over their assets through a hybrid self-custody system, while the credit union adds institutional security measures and reporting functions [1].

In parallel, a banking consortium with significantly larger ambitions is forming in Europe. Qivalis, which has consisted of twelve European major banks since December, is planning to launch a euro stablecoin in the second half of 2026 [2]. The strategic objective is unmistakable: Jan Sell, CEO of Qivalis and former Germany head of Coinbase, speaks of a "regulated, domestic alternative to US dollar-denominated stablecoins" within the EU [2]. The token is explicitly positioned as a counterweight to USDT, USDC, and other dollar-based stablecoins.

The technical concept is deliberately conservative: 1:1 euro peg, at least 40 percent of reserves as bank deposits, the remainder in short-term eurozone government bonds, plus daily redeemability [2]. Sell sees use cases particularly in real-time payments in cross-border business transactions—a market where traditional banking infrastructure is often slow and expensive [2]. Qivalis views MiCA regulation with its strict capital, governance, and transparency rules as a competitive advantage over less regulated providers [2].

Discussions with crypto exchanges, market makers, and liquidity providers are already underway to ensure immediate listing and sufficient liquidity at launch [2]. The participating banks are expected to distribute the token in parallel through their own channels. The motivation is clear: Globally, over 95 percent of stablecoin volume is still tied to the US dollar [2].

Analysis & Context

Both developments reveal a fundamental insight of the traditional financial world: Those who rely on complete outsourcing of digital assets risk their long-term raison d'être. The SCFCU solution and the Qivalis initiative follow different approaches, but share the same strategic premise—control over customer relationships and data sovereignty must not be surrendered to Big Tech companies or specialized crypto providers.

The European initiative is politically explosive. A successful euro stablecoin would not only strengthen Europe's financial sovereignty, but could also challenge the dollar's role in digital payments. The 95 percent dollar dominance in the stablecoin market is no coincidence, but an expression of global currency preferences. Circle (USDC) and Tether (USDT) have earned this position over years by building liquidity, network effects, and trust. Qivalis faces the challenge of breaking these established monopolies—a task at which several projects have already failed.

The timing question is crucial. MiCA as a regulatory framework could prove to be a double-edged sword: On one hand, strict regulation creates trust among institutional users; on the other hand, it could slow innovation and make the token unattractive to global users. The American SCFCU solution shows a more pragmatic path: Instead of creating its own tokens, it integrates existing Bitcoin infrastructure into its own systems. This approach avoids the complexity of reserve management and leverages Bitcoin's already existing liquidity and acceptance.

Historically, established financial institutions have often been too late or chosen the wrong approach during technological disruptions. The success prospects of both models depend on whether they offer genuine added value or merely represent regulatory compliance exercises. Particularly relevant for Bitcoin investors: The more traditional institutions build their own infrastructure for digital assets, the less dependent they become on specialized crypto companies—which could lead to more competition and better conditions in the long term.

Conclusion

• Traditional financial institutions have recognized that outsourcing digital assets to third-party providers endangers their long-term existence—control over customer relationships is becoming a strategic survival question

• The European initiative of a euro stablecoin by twelve major banks is primarily a geopolitical project to reduce dollar dependence, but faces the enormous challenge of breaking through 95 percent market dominance

• The integration of Bitcoin into existing banking systems, as demonstrated by SCFCU, appears more pragmatic than creating new tokens, as it leverages established liquidity and acceptance

• MiCA regulation is becoming a differentiating factor: European providers rely on compliance as a competitive advantage, but simultaneously risk becoming globally unattractive through overly strict rules

• For Bitcoin users, these developments mean more choices in the medium term and potentially better conditions through increasing competition between traditional institutions and crypto-native providers

Sources

AI-Assisted Content

This article was created with AI assistance. All facts are sourced from verified news outlets.